Skip to content

Skip to contentBusiness Advisory

Our Brochure & Company Profile

To read more about the services provided by RBS, please see our detailed brochure and our company profile.

Tags

Business Advisory Services

UAE is the trading paradise of the world. Located strategically in the richest region of the world, UAE has grown to become the best trading port in the world. The market in the UAE and GCC is complex and requires authentic data and information to enable the business to harness the dynamic business environment prevailing in the UAE and GCC. A consulting firm that can give advice and assist in compliance is a must. At RBS we are providing the following advice and consultancy services in Dubai, UAE.

- Economic Substance Regulations (ESR)

- Ultimate Beneficial Ownership (UBO)

- Country by Country Reporting (CbCr)

- Anti- Money Laundering regulation (AML)

Business Advisory (key point)

- Economic Substance Regulations (ESR)

- Ultimate Beneficial Ownership (UBO)

- Country by Country Reporting (CbCr)

- Anti- Money Laundering regulation (AML)

Economic Substance Regulations (ESR)

On August 10, 2020, New Economic Substance Regulations (ESR) was introduced in the UAE via Cabinet Resolution 57/2020 which repealed and revoked Cabinet Decision no. 31/2019. Also, Ministerial Decision No. 100 for the year 2020 replaced Ministerial Decision 215 for the year 2019.

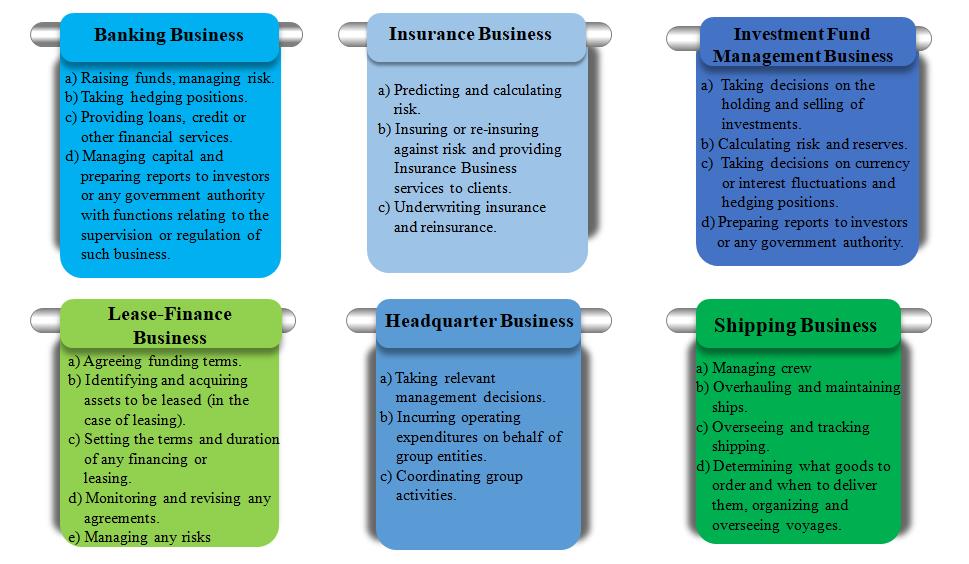

Economic Substance Regulations (ESR) apply to all Licensee & Exempted Licensee carrying on the Relevant Activities in the UAE, including the Free Zone or Financial Free Zone; with effect from the year 2019.

As per the new amendment, a licensee is a juridical person and unincorporated partnerships that carry out a relevant activity under ESR in UAE. For example:

- Limited liability companies

- Private shareholding Company

- Public Shareholding Company

- Partnership (LLP, LP, GP, etc)

- Any other entity with a legal personality separate from its owner

Exempted licensees under ESR: ESR exemption, earlier granted only to entities with 51% or more direct/indirect government ownership, has now been repealed. Under the new ESR, the following categories of licensees will be exempt:

- Investment funds;

- UAE branches of foreign companies;

- Licensees that are tax resident outside UAE;

- UAE resident-owned businesses; and

- Any licensee for which the Minister of Finance issues a decision to grant it a capacity of an ‘exempt licensee’ under ESR.

Exempted licensees that carry out a relevant activity still need to file notification under ESR along with sufficient evidence claiming the exemption.

The requirement to meet Economic Test under ESR

- Check whether the entity conducts/ performs Core Income-Generating Activity (CIGA) in the State.

- Check whether the entity is directed and managed in the State in relation to that activity.

- Check whether the company employs an adequate number of qualified full-time employees or incurs an adequate level of operating expenditure and adequate physical assets in the state.

- If CIGA is conducted by another entity for the relevant licensee, then check whether the Licensee has full control and can monitor the activities of another entity.

Authorities as per CRN 57/2020:

The penalty in case of failure to submit the notification under ESR

An administrative Penalty amounting to AED 20,000 shall be imposed on Licensee or Exempted Licensee who has failed to submit the notification or any information or document required to be filed

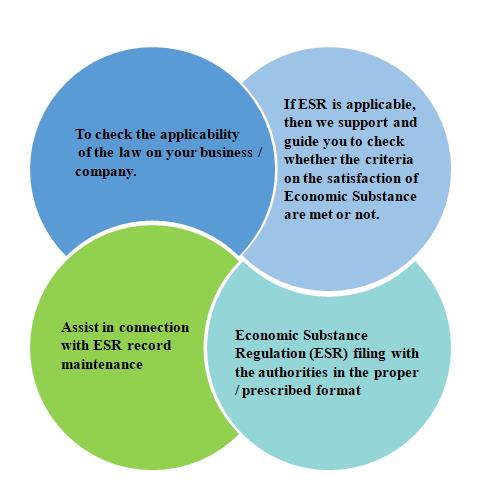

“How RBS can help in ESR compliance”

Ultimate Beneficial Ownership (UBO)

UAE recently replaced Cabinet Decision No. 34 of 2020 with Cabinet Resolution No. 58 of 2020 on the Regulation of the Procedures Related to Real Beneficiaries (“Decision”).

UBO applies to the registrar and legal person such as individual, company, and entity who are licensed or registered in the state, including the commercial-free zones.

Exceptions:

The company’s wholly-owned by the federal or local government or any other companies wholly owned by such companies, and the Financial Free Zones; like ADGM and DIFC.

Why UBO is implemented?

- Maintain UAE’s economic position with International requirements

- To regulate minimum obligations in disclosure of Beneficial Owners, Shareholders, Partners & Nominee Board Members

- To have effective & enduring regulatory mechanism & procedures for the beneficial owner data

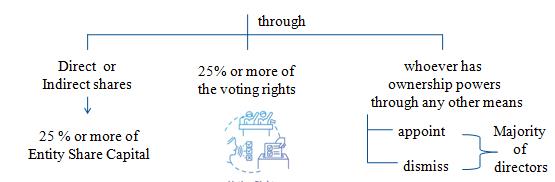

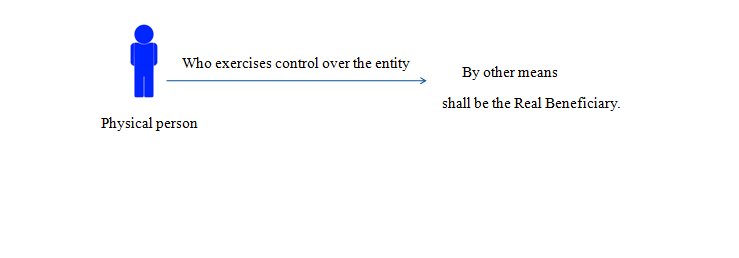

Who are Beneficial Owner or Real Beneficiaries under UBO?

- The person who owns or controls a legal person

- If no Real Beneficiary fits criteria above or any doubt over who has final controlling ownership then

- If no physical person is determined, then the Real Beneficiary shall be the physical person who holds the position of the person in charge of Senior Management.

- If more than one person participates in owning or controlling a share then all of them shall be treated as owners and controllers of such share.

Partners & Shareholders

For the register of partners or shareholders, a company must maintain the details of its partners or shareholders as set out in the UBO Regulations and update such register with any change occurring within 15 days from the date of the change.

The register of partners or shareholders must include certain information, including without limitation, the number of shares held by each partner or shareholder, the voting rights attached to such shares, and the date of acquisition of shares by each partner or shareholder. Information on each partner and shareholder (whether a natural or legal person) listed in the register must also be provided as set out in the Regulations.

Documents to be maintained under UBO

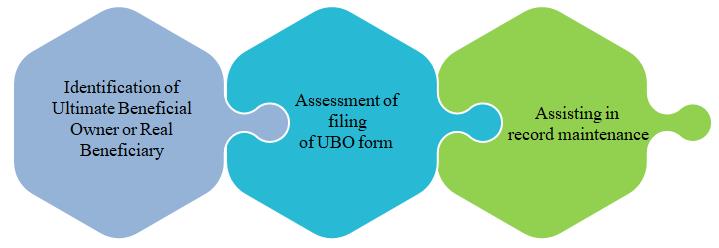

- Real Beneficiary Register

- Partner & Shareholder Register and

- A Registrar of Nominal Members

RBS Services in Dubai, UAE Includes the following :

Country by Country Reporting (CbCr)

CbCr Reporting is part of Action 13 of the Base Erosion and Profit Shifting (BEPS) initiative led by the Organization for Economic Co-operation and Development (OECD) and the Group of Twenty (G20) industrialized nations. It is initially introduced in the United Arab Emirates (UAE) with effect from the year 2019 through Cabinet Resolution No. 32 of 2019, which is now replaced by Cabinet Resolution No. 44 of 2020 and will be in effect.

BEPS Action 13 requires large Multinational Groups of Entities (MNEs) to file a CbCr report that should provide a breakdown of the Multinational Group’s global revenue, profit before tax, income tax accrued, and some other indicators of economic activities for each jurisdiction in which the MNE operates. The purpose of CbC Reporting is to eliminate any gap in information between the taxpayers and tax administrations with regards to information on where the economic value is generated within the MNE Group and whether it matches where profits are allocated and taxes are paid on a global level.

Applicability

Applicability of CbCR Notification

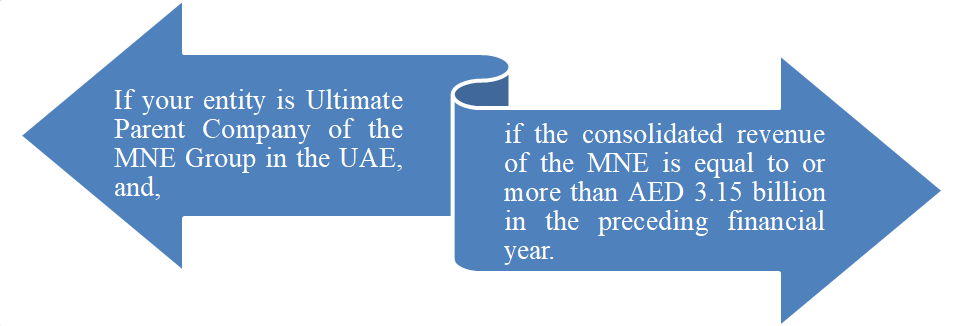

- Each Ultimate Parent Entity of the MNE Group whose tax residence is located in the State shall notify the Competent Authority that it is the Reporting Entity, no later than the last day of the Group’s Reporting Fiscal Year.

- Each Reporting Entity shall submit a report to the Competent concerning its Reporting Fiscal Year on or before the date specified in reporting.

Applicability of CbCR Notification

The report shall be submitted no later than the twelve (12) months grace period after the last day of the Reporting Fiscal Year of the MNE Group.

Contents of the Report

a. Aggregate information relating to

- the amount of revenue,

- profits / (losses) before income tax,

- income tax paid,

- income tax accrued,

- stated capital,

- accumulated earnings,

- number of employees,

- non-monetary or cash equivalent assets,

- tangible assets in respect of each country in which the MNE Group carries out its activities

b. An identification of each Constituent Company of the MNE Group indicating the jurisdiction of tax residence of such Constituent Company, and, where different from such jurisdiction of tax residence, the jurisdiction under the laws of which such Constituent Company is established, and the nature of the main business activity or activities for each such Companies.

Penalties under CbCr

Administrative penalty – Reporting Entity

Administrative penalty – Ultimate Parent Entity

- Fails to provide the notification : AED 1 Million + AED 10,000 for each day that the failure

continues with a maximum of AED 250,000.

Anti – Money Laundering (AML)

The UAE has strengthened anti-money laundering (AML) in recent years. The Federal Law no Federal Decree-law No. (20) of 2018 issued by as per Cabinet Decision along with other rules governs AML in UAE.

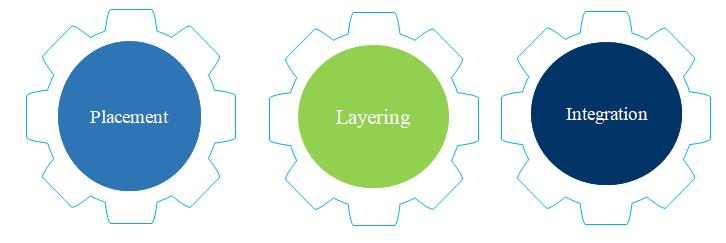

Any person, knowing that the funds are the proceeds of a felony or a misdemeanor, and who willfully commits any of the following acts, shall be considered a perpetrator of the crime of Money Laundering. There are three basic stages of money laundering :

The crime of Money Laundering is considered an independent crime. The punishment of the perpetrator for the predicate offense shall not prevent his punishment for the crime of Money Laundering.

Anti-money laundering (AML) refers to the laws, regulations, and procedures intended to prevent criminals from disguising illegally obtained funds as legitimate income. Though anti-money laundering laws cover a limited range of transactions and criminal behavior, their implications are far-reaching.

Who will be responsible under AML?

The legal person shall be criminally responsible for the crime if it is committed in their name or for its account intentionally, without prejudice to the personal criminal responsibility of the perpetrator and the administrative penalties as prescribed by law

Any person shall disclose whenever he brings into the UAE or takes out any currency or bearer negotiable instruments or precious metals or stones of value, in accordance with the disclosure system issued by the Central Bank.

How to Prevent AML in a firm

- Creating a Strong Compliance Culture

- Designated AML Compliance Officer

- Skilled Compliance Resources

- Clear Roles and Responsibilities

- Regular AML training

- Relationship Survey

- Strong management reporting

- Periodic Testing

Penalties under AML

Fine regarding AML can range from AED 10,000 (ten thousand dirhams) to AED 50,000,000 (fifty million dirhams).

Along with a fine, a term of Imprisonment can range from temporary imprisonment to lifetime imprisonment.

How RBS can help under AML?

- Meeting with employees

- Assess if the firm works along with AML laws and regulations

- If not, then giving guidance to take the necessary steps to follow AML.

- Prepare report if necessary regarding AML reporting and

- Schedule meeting with the management

- Provide ongoing monitoring and support